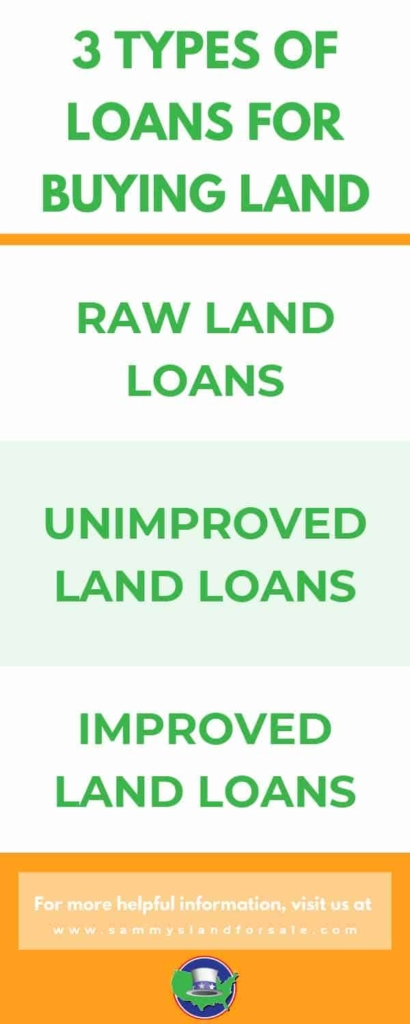

There are many different kinds of loans available for people who want to purchase land, and the main differentiation comes from what type of land you’re looking to purchase. You might be considering raw land, unimproved land, or improved land, and these three different types of land will greatly influence what type of loan you’ll need to get.

There are many different kinds of loans available for people who want to purchase land, and the main differentiation comes from what type of land you’re looking to purchase. You might be considering raw land, unimproved land, or improved land, and these three different types of land will greatly influence what type of loan you’ll need to get.

Raw Land Loans

Raw land is land that is completely untouched by man, so it does not include any connections to utilities, such as:

- Electricity

- Sewers

- Roads

Because this land is completely uncultivated, it can be used for almost anything, as long as the soil type and zoning laws allow for it. Some buyers prefer this, because they are able to purchase the land and then choose what they’d like to use it for, whether it’s residential, recreational, farming, or commercial use.

While raw land was not a popular choice for buyers in the past, landowners have become more aware of its benefits in recent years. It’s no secret that, especially in the United States, raw, untouched land is a scarcity. Even if you don’t have any immediate plans for the land, this factor alone will cause your purchase to increase in value over time. If you do choose to develop it in any way, this will only increase the value of the land more.

Raw land itself may be cheaper to purchase than developed or developing land, but it can be more difficult to get financing for. This is because many lenders view it as a higher risk. Before applying for financing, make sure to draw up a detailed outline for how you plan to use the land. This will show banks that you are committed to the project you’re purchasing the land for, which shows that you don’t pose as big of a risk as people who are underprepared.

Another way to increase your chances of qualifying for a raw land loan is to offer a larger down payment than what’s required and show an excellent credit history. While both a large down payment and good credit history are necessary for procuring any kind of land loan, showing your lender that you have more to offer than others will help increase your chances of approval, especially in the case of raw land.